FROM TENANT TO RENT-FREE: A 30-Year Wealth-Building Framework for the Long-Term Renter

By Neil O. Campbell

Founder & Strategic Thinker

A LIVING ECOSYSTEM DESIGN (LED) STRATEGIC ANALYSIS

Executive Summary

For decades, the American housing narrative has pivoted on a single axis: homeownership. The dominant framework presents buying a home as the primary and often the only legitimate pathway to financial stability, wealth accumulation, and long-term security.

Yet for millions of households constrained by affordability gaps, structural credit barriers, or deliberate mobility preferences, homeownership remains inaccessible or impractical. These renters face a compounding disadvantage: decades of housing expenditure that yield no direct asset accumulation.

The Living Ecosystem Design (LED) Rent Freedom Strategy challenges this premise. It does not ask renters to purchase property. Instead, it offers a systematic, discipline-driven framework for replicating the wealth-building mechanism embedded within homeownership without requiring a deed.

The strategy rests on a straightforward premise: what if renters treated themselves as their own equity partner?

"The question is no longer whether renters can build equity. The question is whether renters can build enough productive assets that they no longer need to pay rent from earned income at all."

The Structural Problem Facing Renters

Modern renters operate within a system defined by three persistent structural challenges:

• Rising rent costs that chronically outpace income growth, eroding disposable income and savings capacity year over year.

• Limited access to homeownership due to tightening credit standards, insufficient down payment reserves, and persistently elevated housing prices in many markets.

• No direct pathway to asset accumulation from monthly housing payments, an asymmetry that compounded over decades, produces significant wealth disparities between renters and owners.

In contrast, homeowners convert a portion of each mortgage payment into equity through principal reduction, a wealth mechanism that compounds invisibly over time. After thirty years, the divergence in net worth between an owner and a renter of equivalent income is not incidental. It is structural.

The LED framework does not attempt to eliminate renting or romanticize property ownership. It identifies a more precise problem: the absence of a parallel wealth-building mechanism for renters and proposes a replicable solution.

Root Cause Analysis

The wealth gap between renters and homeowners is not primarily a consequence of individual financial behavior. It is a consequence of system design.

Mortgage structures compel wealth accumulation by embedding a mandatory savings mechanism, principal repayment into every monthly payment. The homeowner does not require exceptional discipline; the system enforces it.

Renters, by contrast, operate in a system with no equivalent mechanism. Monthly payments leave no residual asset. Without an intentional parallel structure, the financial gap between tenure types widens regardless of how responsibly individual renters manage their finances.

The LED Rent Freedom Strategy addresses this design asymmetry directly by equipping renters with a self-administered framework that replicates the compounding wealth effect of principal accumulation.

The LED Rent Freedom Strategy: A Four-Step Framework

The following four steps constitute the operational core of the LED Rent Freedom Strategy. Together, they convert housing expenditure from a purely consumptive activity into a dual-purpose financial system.

Simulate an Interest-Only Mortgage

Invest the Difference Consistently

Convert Consumption Into Capital

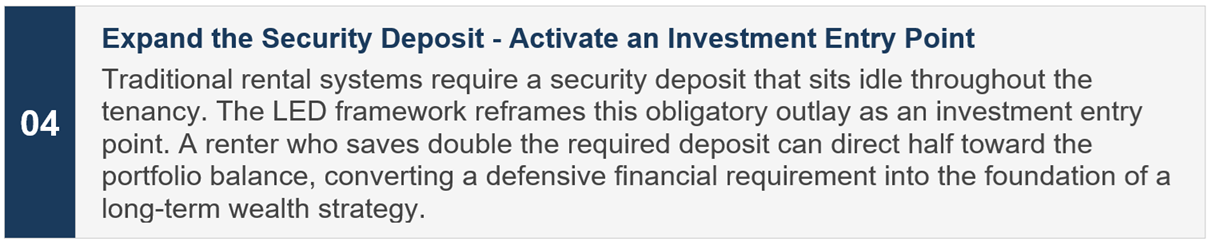

Expand the Security Deposit

Example Deposit Activation:

Allocation illustration

The Power of Compounding: A 30-Year Illustration

To illustrate the potential of this framework, consider the following illustrative scenario:

• Initial investment: $3,200 (activated security deposit)

• Monthly contribution: $300 (self-principal payment)

• Supplemental capital: modest but consistently reinvested cash-back rewards

• Time horizon: 30 years

Applying standard compound growth assumptions across a range of return scenarios produces the following illustrative outcomes:

Annual return assumption graph

These figures are illustrative, not guaranteed. Market returns vary, and past performance does not predict future outcomes. However, they demonstrate a principle that is mathematically well-established: time and consistency can transform relatively small, disciplined contributions into substantial financial assets.

Critically, this portfolio is not designed to purchase a home. It is designed to purchase freedom, the capacity to sustain housing costs from investment returns rather than earned income alone.

"Housing security is not a deed. It is a capability, the financial capacity to maintain housing regardless of employment status or market conditions."

Economic, Social, and Governance Implications

Housing as Retirement Infrastructure

Traditional frameworks define housing as shelter and recurring expense. The LED framework expands this definition fundamentally.

Under this model, housing becomes retirement infrastructure. The strategic objective is to build an asset base capable of:

• Covering future rent obligations from investment income

• Offsetting essential living expenses during retirement

• Providing a financial buffer during income disruptions or career transitions

• Supplementing Social Security or pension income

A renter who follows this approach is not merely paying for housing, they are constructing a financial system that can eventually sustain housing costs independently of their employment status.

Redefining Housing Security

Housing security is commonly equated with ownership. But ownership without liquidity, particularly when leveraged with high mortgage debt and limited cash flow flexibility does not guarantee stability.

Under the LED framework, housing security is defined by financial capability rather than tenure status:

• A renter with a large, income-producing investment portfolio may demonstrate greater resilience than a highly leveraged homeowner with limited savings and cash-flow constraints.

• True housing security is the ability to maintain stable housing regardless of employment status, market conditions, or life transitions.

This reframing matters not only for individual financial planning but for how policymakers, lenders, and institutions assess and support housing stability across diverse populations.

Broader Policy and Market Considerations

The Rent Freedom Strategy raises consequential questions for institutions, employers, and policymakers:

• Should financial literacy programs explicitly teach renter wealth-building strategies alongside conventional homeownership guidance?

• Could employers offer Rent Freedom investment-matching programs as a workforce benefit, analogous to 401(k) employer matching?

• Might apartment communities and property management platforms integrate investment tools directly into their leasing and resident experience infrastructure?

• Could municipalities and regional economic development strategies incorporate renter wealth-building as a formal component of household resilience policy?

As long-term renting becomes an enduring reality for a growing share of the workforce, not merely a transitional phase, these questions move from theoretical to urgent.

The Case for Action

Every month a renter spends without a parallel wealth-building strategy is a month of compounding opportunity cost. The mathematics of long-term investing are unforgiving in both directions: those who begin early benefit disproportionately, and those who delay pay a compounding penalty.

The LED Rent Freedom Strategy requires no exotic instruments, no specialized access, and no minimum income threshold beyond basic affordability. It requires consistency, a reframe of purpose, and a commitment to treating housing expenditure as a catalyst rather than a ceiling.

The barriers to implementation are primarily conceptual, not financial. The framework is accessible to any renter willing to apply disciplined, systematic thinking to an expenditure they are already making.

Implementation Considerations

The following practical considerations support effective adoption of the framework:

• Begin with an honest assessment of current housing costs, income, and discretionary capacity to identify a realistic self-principal contribution amount.

• Select low-cost, broadly diversified investment vehicles such as index funds to minimize fees and maximize long-term compounding efficiency.

• Automate contributions to replicate the mandatory savings mechanism embedded in mortgage structures, removing the need for active monthly decision-making.

• Establish clear reward-reinvestment protocols at the outset to prevent cash-back and passive rewards from being absorbed into general spending.

• Review and recalibrate the strategy annually as income, housing costs, and life circumstances evolve.

Note: The financial projections presented in this framework are illustrative scenarios based on mathematical modeling. They are not financial advice, and individual outcomes will vary based on market conditions, contribution consistency, investment selection, and personal circumstances. Readers are encouraged to consult a qualified financial professional before implementing any investment strategy.

Conclusion: A Third Path

The future of housing does not require a binary choice between renting and wealth creation.

The LED Rent Freedom Strategy introduces a third path, one in which the discipline of housing payments fuels the construction of a parallel asset portfolio capable of funding future rent, strengthening retirement security, and increasing long-term financial resilience.

This is not a speculative proposition. It is a systems-design solution to a design asymmetry, one that has disadvantaged renters not because of their choices, but because of the architecture of the financial systems surrounding them.

The LED framework offers a path forward: systematic, replicable, and accessible. The question renters must now confront is not whether they can build wealth. It is whether they are willing to begin.

"Use the discipline of housing payments to build a parallel asset portfolio,one capable of funding future rent, strengthening retirement security, and increasing long-term resilience."

ABOUT THE AUTHOR

Neil O. Campbell | Founder & Strategic Thinker | Living Ecosystem Design (LED)

Neil O. Campbell is a systems strategist and the Founder of Living Ecosystem Design (LED), a strategic framework and initiative dedicated to aligning physical design, governance, capital, infrastructure, and human systems to create resilient, thriving communities. Campbell's work focuses on identifying overlooked assets, redesigning fragmented systems, and improving the long-term health and productivity of communities and institutions.

The Rent Freedom Strategy represents one dimension of the broader LED mission: applying systems-thinking and interdisciplinary frameworks to economic challenges that have resisted conventional solutions. Campbell's work is grounded in the conviction that durable community prosperity requires not the optimization of isolated components, but the redesign of the systems connecting them.

© Living Ecosystem Design (LED). All Rights Reserved.